Transforming financial infrastructure for inclusive growth

2024

Credicorp / Banco de Crédito del Perú + Institute of Design at Illinois Tech

Enabled Credicorp to size a $9.8B market by reframing embedded finance around informal capital, co-designed trust metrics, and eligibility reform. Delivered nine investable tools and a scaling roadmap supporting regional adoption. Positioned equity as a commercial growth lever, transitioning embedded finance from transactional access to systemic infrastructure shaping LATAM subsidiary strategies.

28.6%

CAGR

$9.8B

50%

Unbanked

Over half of Latin America's population remains excluded from formal finance despite growing digital adoption, representing a $9.8B market opportunity. Over half of Latin America’s population remains excluded from formal finance due to systemic gaps in identity, infrastructure, and institutional trust. Embedded finance reframed from a digital access tool into a trust-based system that validates informal capital, redefines eligibility, and activates community-rooted participation. Designed to shift exclusion patterns into scalable investment pathways grounded in long-term value.

Metric | Definition | Value (USD) |

|---|---|---|

Total Addressable Market (TAM) | Total Latin America embedded finance market size (2024) | $9.8B |

Serviceable Available Market (SAM) | Credicorp’s regional fintech scope (~7.5% of LATAM TAM) based on operations in Peru, Colombia, Chile, Bolivia | $735M |

Serviceable Obtainable Market (SOM) | Realistic capture (~25% of SAM) due to infrastructure, user base, and regulatory trust | $184M |

Growth context: LATAM embedded finance market project to grow to $34.5B with 28.6% CAGR by 2029

Source: Sources: Research and Markets (2024); Business Wire (2024); Finnovista Fintech Radar Peru (2024); BCG & Adyen Embedded Finance Study (2024); Statista (2024)

Surface —

Cashless transitions create a paradox for Latin American financial institutions: while digital adoption accelerates, over 50% of the population remains excluded from formal finance. Cashless transitions risk reinforcing structural exclusion. Over 50% of Peru’s population remains unbanked due to breakdowns in infrastructure, identity verification, and institutional trust, as surfaced through stakeholder interviews. Financial products operate on outdated assumptions, including requirements for formal income documentation or traditional credit histories, which misalign with user realities.

A three-capital assessment revealed how deficits in social networks, digital fluency, and equitable institutional access block eligibility. Stakeholder mapping identified misalignments between financial models and lived community patterns.

Co-design workshops highlighted behavioral cues ignored by conventional systems. Informal capital surfaced as untapped infrastructure. Inclusive finance requires systems that treat lived behaviors as credible inputs, redefining eligibility to support trust-based participation at scale.

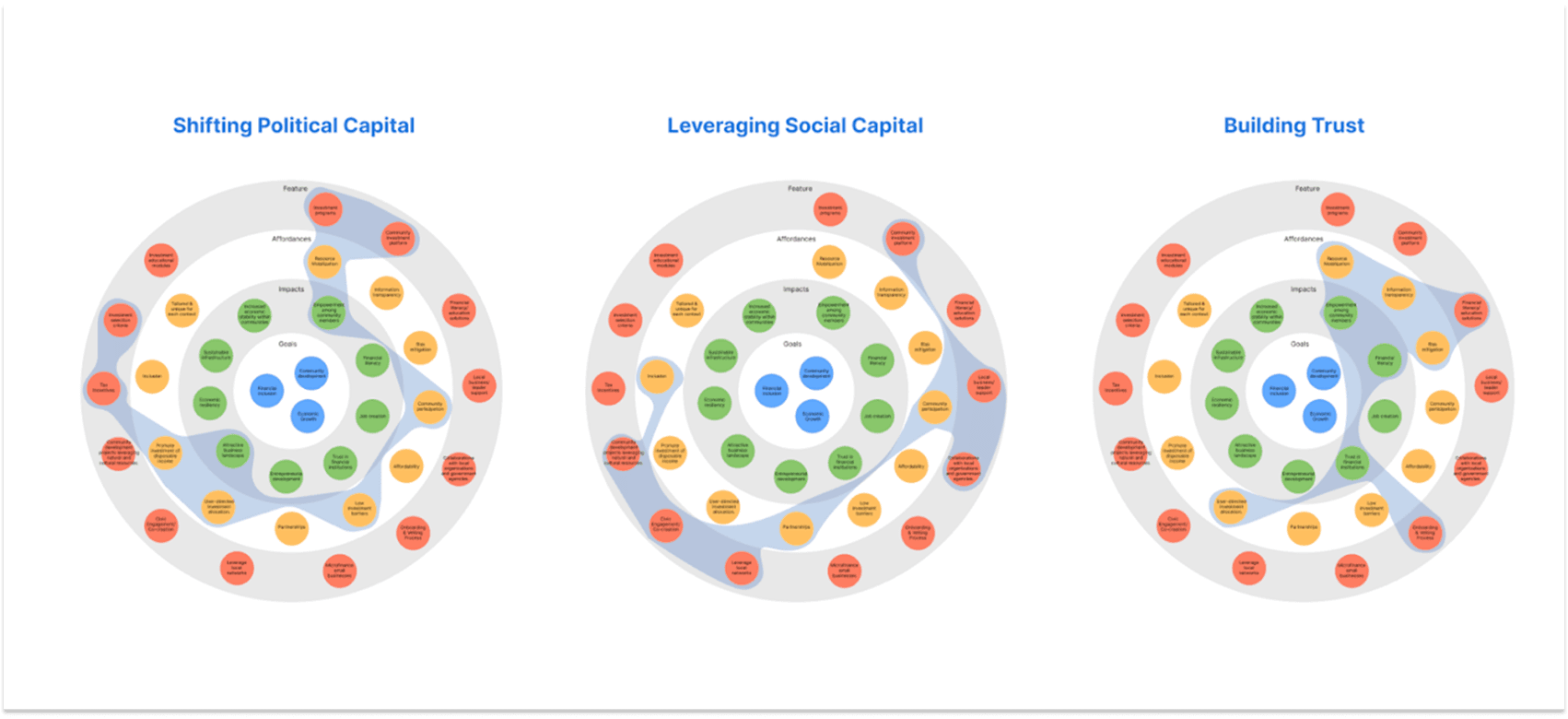

Shift —

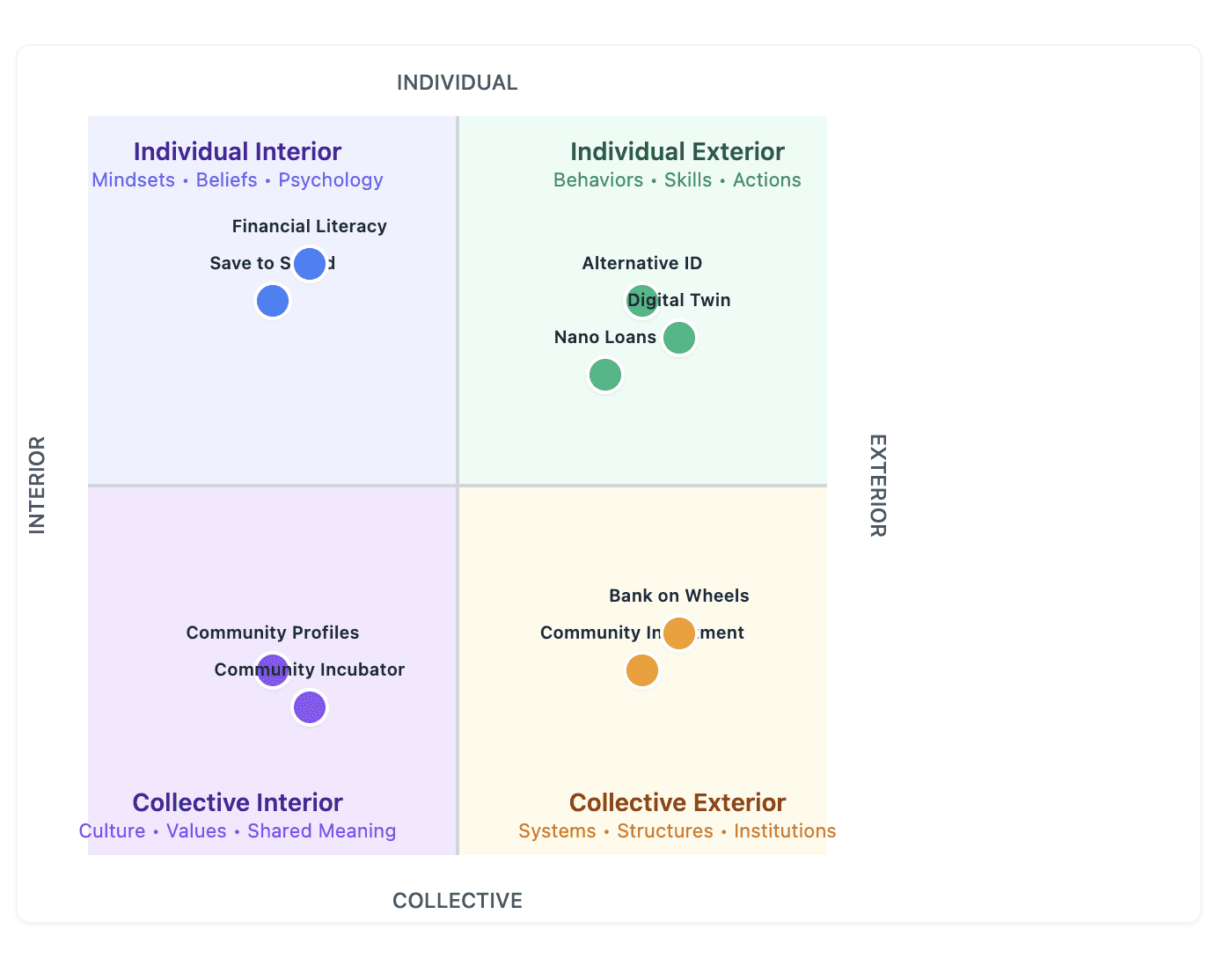

Hypothesis-led archetypes addressed exclusion through three capital levers: social, institutional, and human. Each archetype linked to solutions co-developed during stakeholder workshops.

Archetypes and Solutions

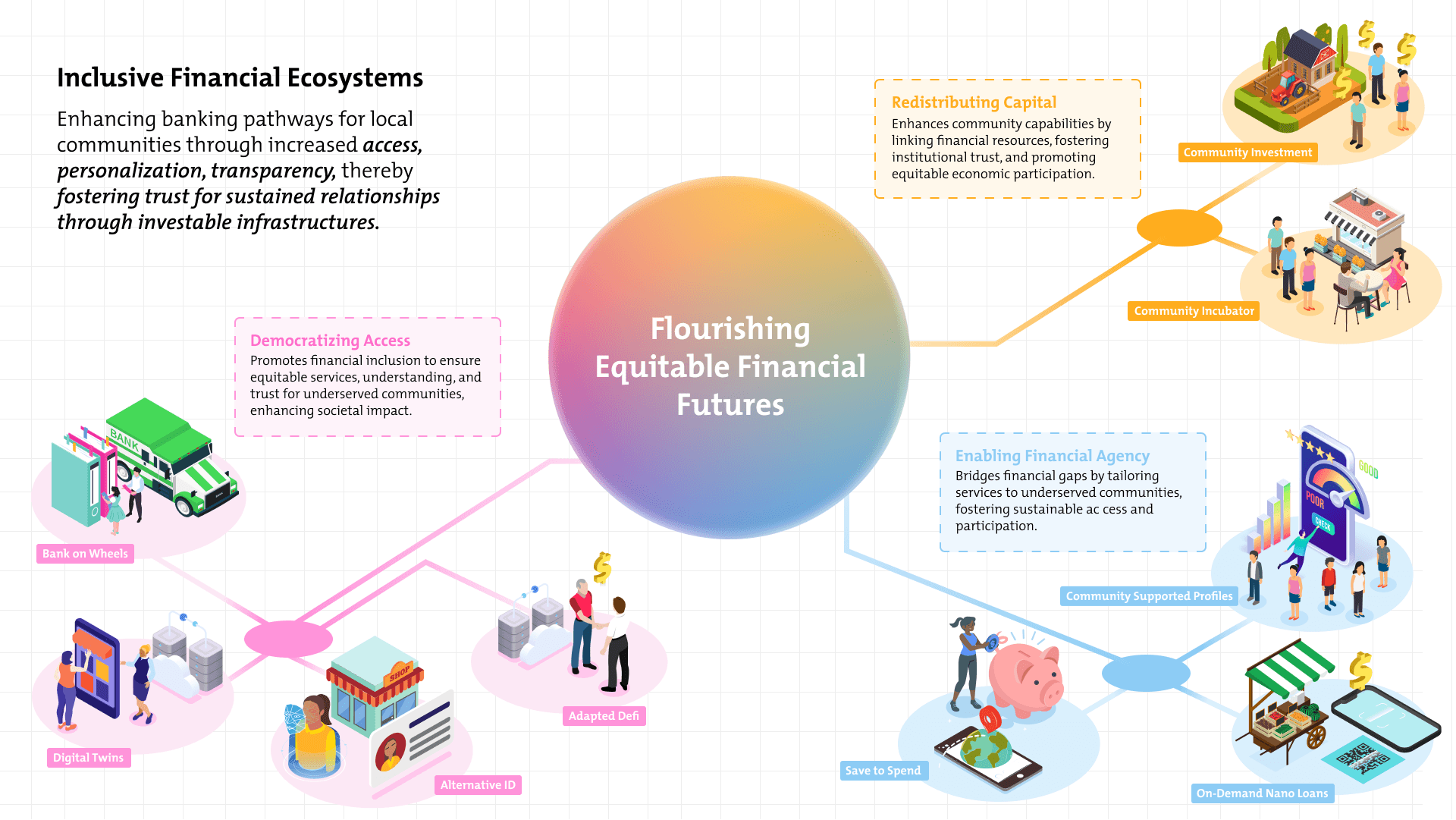

• Enabling Financial Agency → Community Profiles, Nano Loans

• Redistributing Capital → Community Investment Platforms, Save to Spend

• Democratizing Access → Digital Twin, Alternative ID, Bank on Wheels

Enabling Financial Agency

Feature (MVP) | Functionality | Validation Metrics (need update) |

On-Demand Nano Loans | Real-time, low-interest loans for essentials at point-of-sale | Repayment rates, credit access for new users |

Save to Spend | Suggests savings during non-essential purchases via geolocation | Savings frequency, emergency fund growth |

Community-Supported Profiles | Credit scoring from rent/utilities & peer endorsements | New credit users, repayment stability |

Redistributing Capital

Feature (MVP) | Functionality | Validation Metrics |

Community Incubator | Shared tools & mentorship for small business growth | Business survival, job creation, literacy gain |

Community Investment (Crowdfunding) | Crowdfunded platform for local, impact-driven investments | Funds raised, investor ROI, community engagement |

Democratizing Access

Feature (MVP) | Functionality | Validation Metrics |

Alternative ID Card | Financial ID for unbanked/undocumented individuals | ID issuance, account openings, credit history built |

Adapted DeFi | Decentralized tools for loans, payments, savings without intermediaries | User growth, transaction volume, cost savings |

Bank on Wheels | Mobile unit providing banking services and financial education | New accounts, literacy outcomes, use by first-time users |

Digital Twin | Safe simulator for practicing personal finance decisions | Knowledge gain, real-world financial behavior improvement |

Interventions evaluated for feasibility, desirability, and viability using co-created criteria. Strategic trade-offs modeled with risk-reward matrices aligned to institutional priorities and community conditions. The resulting framework aligned embedded finance innovations with Credicorp’s regional expansion strategy while directly addressing systemic exclusion.

Sustain —

Sustainable adoption requires coordinated activation across three stakeholder groups, each with distinct implementation capabilities and success metrics.

Multi-stakeholder coordination through structured co-design sessions aligned solutions with real implementation challenges. Process engaged BCP leadership and field experts to identify adoption barriers and secure institutional commitment around community-centered financial inclusion. Risk mitigation prioritized integration with existing social capital systems, enhancing community relationships while avoiding disruption of informal networks. Workshops addressed technical feasibility, social acceptance, and institutional capacity. Outputs established a foundation for expansion, with stakeholder coordination model designed for replication across markets while allowing local customization.

Sight Note —

Financial exclusion reflects systemic design flaws rather than user deficits. “Unbanked” status often signals invisibility within existing frameworks.

Trust functions as a strategic asset enabling adoption and sustained participation. Validating community trust transforms financial engagement into reciprocal investment.

Sustainable equity depends on investability. Reducing risk through solutions that align with lived community conditions enables scalable value creation.

https://www.weforum.org/stories/2025/04/embedded-finance-disruptive-force-financial-institutions/